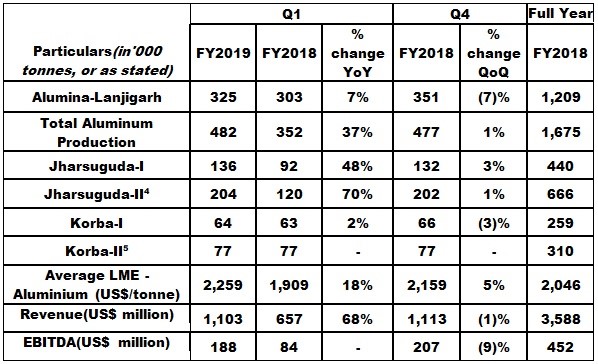

Vedanta Resources releases Production and Financial Results for the First Quarter ended 30 June 2018. The company reports record quarterly aluminium production at 482,000 tonnes, up 37% YoY and commencement of Odisha bauxite delivery to its refinery.

The Lanjigarh refinery produced 325,000 tonnes of alumina in Q1 FY 2019, 7% higher YoY, however 7% lower QoQ due to a temporary break down in the bauxite handling unit.

{alcircleadd}

The increase in aluminium production in Q1 FY2019 was primarily driven by ramp up at the Jharsuguda-II smelter. Other than Line 4, which is still under evaluation, all other lines are expected to be fully ramped up by H1 FY2019. Stabilised aluminium production (i.e. production excluding trial run) was 469,000 tonnes in Q1 FY2019 with an exit monthly run rate of 1.9 tonne per annum.

The cost of production for hot metal in Q1 FY2019 was US$ 1,934 per tonne, 12% higher YoY. The increase was primarily due to increased input cost across imported alumina, coal, caustic and carbon. However, there was a US$ 36 per tonne reduction in price from Q4 FY2018 primarily due to local currency depreciation and operational savings. Power imports and input cost inflation partially offset the other factors.

The company is negotiating with Coal India for domestic coal procurement to improve e-auction coal availability and also focussing on increasing linkage through auction.

Revenue for Q1 FY2019 increased 68% YoY to US$ 1,103 million on higher production and LME prices. EBITDA for the quarter also increased to US$ 188 million YoY on account of higher volumes and LME prices, partially offset by higher cost of production.

The company continues with its previous production guidance of 2 million tonnes of aluminium and 1.5-1.6 million tonnes of alumina in FY2019. The company expects alumina production to ramp-up in the coming quarters supported by availability of higher quality Odisha bauxite. The company targets a drop in cost of production by US$120-170/t in FY2019 from FY2018 average through cost optimization.

Responses