Alumina market witnessed a controlled price trend in 2020 as there had been a fair balance between production and consumption of the ore, even amid the unprecedented COVID-19 pandemic. In the first few months of the year, the prices trended down significantly due to lower buying interests among primary aluminium smelters, but later on, recovered with market resilience. Australian alumina FOB price closed the year on a bullish trend from US$ 278.50 per tonne to US$ 302 per tonne.

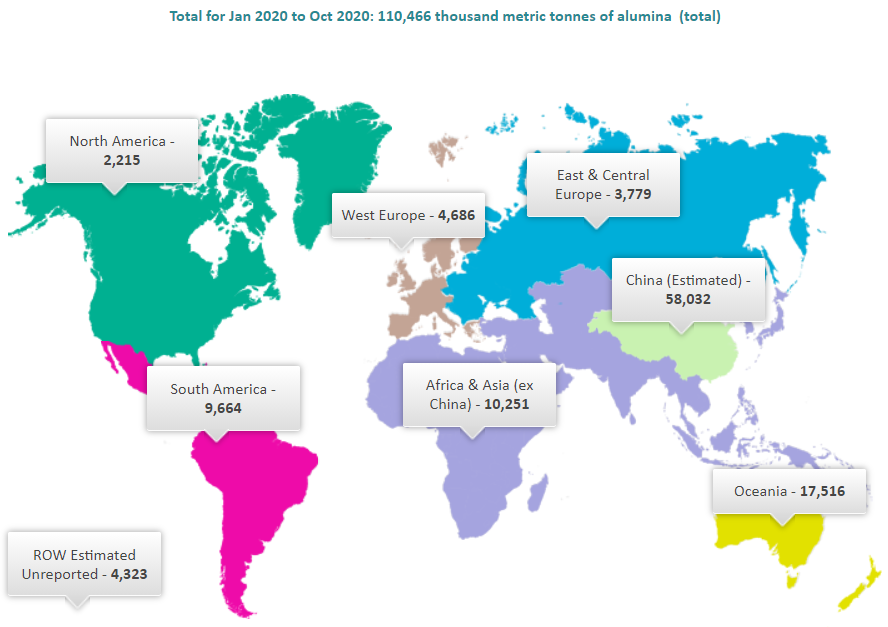

Global alumina output during January-October 2020 stood at 110.466 million tonnes, slightly up by 0.55 per cent from 109.866 million tonnes during the same period last year. Metallurgical-grade alumina production came in at 104.068 million tonnes. Except in China, where alumina production dwindled during the above mentioned period by 2.78 per cent year-on-year to 58.032 million tonnes, the output increased in Africa & Asia (ex-China), East & Central Europe, and also in South America. In Africa & Asia (ex-China), alumina production stood at 10.251 million tonnes, 19.63 per cent more than 8.569 million tonnes during the corresponding period last year. East & Central Europe produced 3.779 million tonnes, up by 2.91 per cent from 3.672 million tonnes last year; while South America churned out 9.664 million tonnes, 10.62 per cent higher than 8.736 million tonnes. In the Oceania region, the second-highest alumina producer after China, produced 17.516 million tonnes during January-October 2020, compared to 16.970 million tonnes a year ago.

{alcircleadd}

World Alumina Production: IAI

Steady alumina production amid sluggish demand during the first few months in 2020 due to the pandemic, coupled with last year's surplus market, led to a global alumina price fall until it started recovering from late April.

Price Scenario

Australian alumina FOB price started the year from January 2 with a growing trend from US$ 278.50 per tonne to US$ 304 per tonne, as of March 13. However, it fell sharply within a month to as low as US$ 225 per tonne. From late April, the price started resonating to reach US$ 302 per tonne, as of December 24, driven by primary aluminium smelters’ stocking of the ore due to low prices. Similarly, the average imported alumina price in China slipped to US$ 317.46 per tonne in late April after rising till the first week of March from US$ 382.44 per tonne to US$ 394.68 per tonne. From April 28, the price started growing to reach US$ 367 per tonne, as of early September, but again fell to US$ 357.44 per tonne by December 24. So, the imported alumina price in China recorded a plunge of 6.54 per cent this year.

Australian Alumina FOB Price

China’s domestic alumina spot price also dwindled this year from US$ 372.79 per tonne to US$ 356.59 per tonne, as shown by the Shanghai Metals Market’s data. Lower production of the ore in China this year failed to pull up the domestic prices. Only in an intermittent period during July, China’s alumina spot price registered a hike to US$ 381.68 per tonne, driven by temporary shutdown of one of Huaxing alumina refinery’s production lines. According to market estimates, the temporary closure of the production line removed around 50,000 to 80,000 tonnes of alumina supply from the Chinese domestic market.

Demand & Supply Scenario

The alumina production in Iran recorded a 4 per cent rise during the first seven months of the current Iranian calendar year (March 20-October 21), compared to the same period of the previous year. Iran Alumina Company in the north-eastern province of North Khosaran, the only alumina refinery of the country, produced 139,307 tonnes of alumina during the said period. Concurrently, the monthly alumina production in the seventh month of this year reached 17,616 tonnes, which illustrates a rise of 6% from the figure for the same month in the previous year.

Alcoa in the third quarter of 2020, ending on September 30, produced 3.435 million tonnes of alumina, up by 1.9 per cent quarter-on-quarter from 3.371 million tonnes. Third-party shipments also rose from 2.415 million tonnes in Q2 to 2.549 million tonnes in Q3. The Company expects its 2020 shipment outlook for alumina to improve by 0.2 million tonnes to between 13.8 and 13.9 million tonnes due to improved production levels.

Pinjarra Refinery

In July 2020, Emirates Global Aluminium achieved the nameplate capacity of 2 million tonnes of alumina production at its Al Taweelah alumina refinery within 14 months since the production began. This capacity is adequate to meet 40 per cent of EGA’s alumina needs and replace some imports.

Hydro in the third quarter results reported that its Alunorte alumina refinery was ramping up production to nameplate capacity. On August 18, Hydro halted operation of the pipeline transporting bauxite from Paragominas to Alunorte for extended maintenance to replace a section of the pipeline earlier than planned, temporarily halting production at Paragominas and reducing production at Alunorte to 50 percent of full capacity. On October 8, Paragominas resumed production and Alunorte started increasing production to nameplate capacity of 6.3 million tonnes.

Rio Tinto’s alumina production is expected to increase from 7.7 million tonnes in 2019 to 7.8 to 8.2 million tonnes during 2020. The company was investing $51 million in upgrading facilities at its Vaudreuil alumina refinery in Quebec, Canada. According to the report, three new energy efficient buildings were under construction.

On the other hand, the government of the Indian State Andhra Pradesh permitted Anrak Aluminium Limited to commission its alumina refinery at Rachapalli, Makavarapalem in Visakhapatnam.

In China, alumina market may see a supply deficit of 361,000 tonnes in 2020, with annual average operating rate at refineries at 78.03 per cent, commented Joyce Li, senior analyst at SMM. Li mentioned that there were 68.65 million tonnes of alumina capacity in operation as of early December among 88.4 million tonnes per year of existing capacity.

Trade Focus

According to the data released by Brazil’s economy ministry in July, alumina exports from Brazil increased in June, albeit at a slower pace than the earlier month. Brazil’s alumina exports in June totalled 679,914 tonnes, up 4.6 per cent year-on-year from 650,229 tonnes. On a month-on-month basis, the exports in June fell by 12.8 per cent from 779,694 tonnes. As per the report, the lower export volumes were attributed to a fall in supply from Hydro’s Alunorte alumina refinery in June due to movement restrictions imposed for containing the spread of the novel coronavirus. Also, 50-70 per cent of Alunorte’s output capacity cut due to power outage at Hydro’s Paragominas bauxite mine could be a reason for the downfall in aluminium ore supply from the refinery. Up until May, Brazil’s alumina export growth rates had been at least 30 per cent up every month on an annual basis.

Lockdown across the world due to the COVID-19 pandemic during July 2020 literally led to a dump of alumina into China. In July 2020, China imported 417,263 tonnes of alumina, more than double the 200,000 tonnes in the year ago, according to Chinese customs data. China’s total alumina imports since the beginning of the year amounted to 2.33 million tonnes, up 341.2 per cent from the corresponding period last year. The stupendous hike in Chinese alumina imports reportedly blew the domestic alumina market, which was already under pressure due to the lack of buying interests among domestic primary aluminium producers.

During January-October, China imported 3.15 million tonnes of alumina, up 205.15 per cent year-on-year. By the end of the year, China’s alumina imports are expected to peg at 3.93 million tonnes, anticipated Li.

_0_0.jpg)

Short Term Outlook

Joyce Li, senior analyst at SMM, anticipated 2021 to be a peak year for the commissioning of alumina capacity in China, while overseas oversupply to intensify and the pressure to increase.

Responses